Why Health Insurance is Non-Negotiable for the Gig Economy

Navigating health insurance without an employer? Explore ACA Marketplace plans, short-term coverage, HSAs, and health sharing ministries for freelancers and gig workers to maintain financial and physical security.

The defining characteristic of being a freelancer or a gig worker is autonomy over time, but this often comes at the cost of job security and, crucially, health benefits. Unlike salaried employees who receive employer-sponsored group insurance with subsidized premiums and low deductibles, freelancers must navigate the healthcare system on their own. This lack of a safety net is a leading cause of financial vulnerability for independent contractors.

For a freelancer, income can fluctuate wildly based on client acquisition, seasonality, or global market shifts. If you become ill, a gap in coverage can turn a manageable medical issue into a financial catastrophe. Without an employer to subsidize the cost, the price of health insurance feels like a mandatory, fixed monthly overhead that can consume a significant portion of net income.

However, this financial burden is manageable with the right strategy. The key lies in understanding the different layers of coverage available in the United States. From the robust protections of the Affordable Care Act (ACA) to the more flexible, albeit limited, options of short-term plans and health-sharing ministries, there are solutions tailored to the irregular income patterns of the gig economy.

The ACA Marketplace: Stability and Subsidies

The most reliable and legally compliant path for freelancers is the Health Insurance Marketplace (often referred to as the Exchange), established under the Affordable Care Act (ACA). This government-regulated marketplace allows individuals to compare plans side-by-side, shop for competitive prices, and determine eligibility for premium subsidies based on their projected annual income.

Key Benefits for Freelancers

- Risk Pools: These plans pool risk across millions of people, ensuring that everyone pays into a fund that covers everyone's medical needs. This means your premiums are spread out over the entire system, making them generally more affordable than self-insured options.

- Essential Health Benefits (EHBs): ACA-compliant plans must cover a standard set of essential health benefits, including:

- Ambulatory patient services (outpatient doctor visits)

- Emergency services

- Hospitalization

- Maternity and newborn care

- Mental health and substance use disorder services

- Prescription drugs

- Laboratory services

- Preventive and wellness services

- Pediatric services

- Reproductive health services for women

- Assistive technology and devices for individuals with disabilities

- No Pre-existing Condition Exclusions: Unlike other types of plans, ACA plans cannot deny coverage or charge higher premiums based on your medical history.

Navigating the Marketplace

The Open Enrollment Period typically runs from November to January for the following calendar year. During "Special Enrollment Periods," you can purchase or change coverage within 60 days of a qualifying life event (e.g., losing coverage, moving, or marriage).

Subsidies and Cost Control

The most critical tool for freelancers is the subsidy. The government calculates your monthly premium based on what a "family at 100% of the federal poverty level" would pay in your area. If your income is below 400% of the federal poverty level, you likely qualify for a premium tax credit.

- Catastrophic High-Risk: If you cannot afford a plan with a low deductible, you might opt for a catastrophic plan (if eligible), which has a higher deductible but lower premium. This is designed for young people or those with financial hardship, but it is generally not recommended for freelancers with high risk.

- Cost-Sharing Reductions (CSR): If your income is between 100% and 250% of the federal poverty level, you may qualify for a Cost-Sharing Reduction. This lowers your deductibles and out-of-pocket costs (copays, coinsurance), which is crucial for a freelancer whose income might drop during a lean month.

Short-Term Health Insurance Plans: Pros and Cons

Short-term health insurance plans are a popular but controversial option for freelancers. They offer lower premiums and fewer exclusions, making them attractive for those trying to save money on overhead.

The Promise of Short-Term Plans

- Lower Premiums: Because they do not cover pre-existing conditions or guarantee issue, premiums are significantly cheaper than ACA Marketplace plans.

- Flexibility: They allow you to customize your coverage amount and duration (often 1-12 months) to match your specific income fluctuation.

- No Pre-Existing Condition Exclusions: Some plans allow you to buy and sell coverage without waiting periods for pre-existing conditions, provided you buy within a specific window.

The Risks and Limitations

- Limited Coverage: Most short-term plans exclude pre-existing conditions. If you get sick with a condition you had before the plan started, they may deny the claim.

- Benefit Caps: Short-term plans often have a maximum benefit cap (e.g., $2 million total). If you incur $500,000 in medical bills, the plan will only pay $2 million, but if you have multiple conditions or a rare condition, the cap could be hit quickly.

- Reimbursement Only: They often pay out-of-pocket for medical bills rather than covering the full cost of care upfront. This requires you to have cash reserves to pay your doctor first and get reimbursed later.

- State-Specific Rules: Some states prohibit or heavily restrict short-term plans. It is crucial to check if your state allows these policies and what the specific restrictions are.

When to Consider Short-Term

Short-term plans are best used for:

- Coverage Gaps: Transitioning from a previous job or plan.

- High-Risk Periods: If you expect a short-term medical emergency (e.g., waiting for a specific treatment) and can afford to self-pay.

- Income Volatility: If you anticipate a period of low income and need to reduce fixed monthly overhead costs.

Warning: Do not use short-term plans as a permanent replacement for ACA coverage. They are generally designed for short-term needs.

Health Savings Accounts (HSAs): The Triple-Tax Advantage

If you have access to a High-Deductible Health Plan (HDHP), you should strongly consider opening a Health Savings Account (HSA). An HSA is a tax-advantaged savings account that you can use to pay for qualified medical expenses.

The Triple-Tax Advantage

- Tax Deduction: Contributions to the HSA are tax-deductible, reducing your taxable income.

- Tax-Free Growth: Earnings on the HSA grow tax-deferred, similar to a 401(k).

- Tax-Free Withdrawals: Money withdrawn for qualified medical expenses is tax-free. If you use it for non-medical expenses, you pay income tax and a penalty.

How It Works for Freelancers

For a freelancer, an HSA is a powerful tool for budgeting. You can contribute to the HSA every time you earn income (up to your annual limit). If your income is high during a tax year, you can contribute the maximum amount. If your income drops next year, you simply don't contribute. This makes the HSA a flexible "medical savings account" that you own, not your employer.

HDHP Requirements

To be eligible for an HSA, you must be enrolled in a High-Deductible Health Plan (HDHP). These plans generally have:

- High Deductibles: Often starting at $1,500 for an individual plan (for 2024).

- Low Premiums: You pay very little in monthly premiums compared to PPO plans.

- Out-of-Pocket Maximums: The plan caps your out-of-pocket costs at a specific amount (e.g., $7,500 for an individual).

Why It Matters

Even if you don't use the money during the year, the money remains in your HSA indefinitely. It becomes your "healthcare nest egg" for when you retire. If you leave a job with a low-deductible plan, you might need to pay for everything out-of-pocket until the deductible is met. An HDHP + HSA allows you to save for those high costs while keeping your monthly overhead low.

Health Sharing Ministries: Faith-Based Alternatives

For those with strong religious convictions, health sharing ministries (such as Christian Healthcare Sharing Ministries, Samaritan Ministries, or Mercy Ministries) offer an alternative to traditional insurance. These are not insurance; they are a form of cost-sharing among members.

How It Works

You contribute a monthly share based on a specific plan (e.g., $100 per month). If you need care, you share that cost with other members.

Pros

- Lower Costs: Premiums are significantly lower than ACA plans.

- Faith-Based: Some ministries provide spiritual support alongside medical coverage.

- No Pre-existing Condition Denials: Some ministries allow you to share the cost of pre-existing conditions, though there may be a waiting period.

Cons

- Not Insurance: They are not subject to state insurance regulations. They can deny coverage or change terms without notice.

- Exclusions: Many exclude specific treatments (e.g., gender-affirming care, certain mental health treatments, or experimental procedures).

- Financial Instability: If the ministry's fund runs low, it may not be able to pay claims.

- State Availability: Some states prohibit health sharing ministries.

Consideration

If you choose this route, ensure you understand the difference between a "sharing" program and an "insurance" plan. Read the fine print carefully to understand what is covered and what is excluded.

COBRA and State Continuation Plans

If you are a freelancer who has just lost a job or stopped working for a company, COBRA (Consolidated Omnibus Budget Reconciliation Act) may be your temporary solution.

What is COBRA?

COBRA allows you to keep your employer-sponsored health insurance for up to 18 months after you lose coverage (or 36 months in some states).

Cost

You must pay the full premium (employer's portion + your portion), which can be a significant financial burden. It is usually more expensive than Marketplace plans, making it a temporary bridge.

State Continuation

Some states offer their own continuation coverage plans if you are not eligible for COBRA (e.g., independent contractors who were misclassified as employees). Check with your state's Department of Insurance.

Use Case

Use COBRA only if you need to maintain the same coverage while you are shopping for a new plan or waiting for a new job to offer benefits. It is generally not recommended as a long-term solution due to the high cost.

Common Pitfalls for Freelancers

- Underestimating Income for Subsidies: When applying for a Marketplace plan, you must provide proof of income for the entire year (including your spouse's). If you are self-employed, use your net profit from your business. Underestimating your income to get a larger subsidy is fraud; overestimating it results in paying more in premiums.

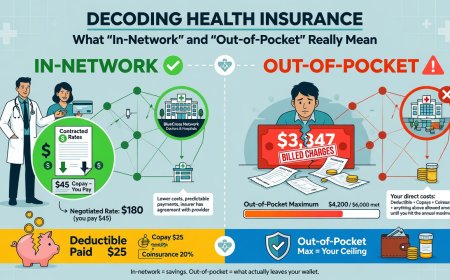

- Ignoring Network Restrictions: Make sure the plan you choose has a "network" that includes your preferred doctors. If you go out-of-network, you may be denied coverage or charged exorbitant fees.

- Confusing "Short-Term" with "ACA": Never buy a short-term plan thinking it is an ACA plan. They are fundamentally different.

- Neglecting Preventive Care: ACA plans cover preventive care (e.g., annual checkups, flu shots) at no cost to you. Don't skip these visits, as early detection saves money in the long run.

- Not Reviewing Policies: Health insurance policies are complex. Read your policy documents to understand what is covered and what is excluded.

Bottom Line: Secure Your Health, Secure Your Future

Navigating the health insurance landscape as a freelancer or gig worker is a challenge, but it is not insurmountable. The stability of your health insurance should never be dependent on your income. By using the ACA Marketplace to access subsidies, considering a Health Savings Account (HSA) to manage out-of-pocket costs, and understanding the limitations of short-term plans, you can build a robust healthcare strategy.

Remember, healthcare is an asset, not a liability. Investing in a plan that covers your needs now can save you thousands of dollars in the future. Don't let the fear of high costs keep you from securing the health you deserve.

Frequently Asked Questions

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

At KREATOR, we are building a hub for original content. We believe that quality ideas deserve to be seen and that writers deserve to be paid for their effort. This is a space where you can showcase your research, share your hobbies, or post your professional skills. By publishing here, you are contributing to a community where ideas matter. Subscribe to our newsletter, read the latest articles, and remember: your voice is valuable. Let’s build something great together.

Comments (0)