How to Avoid Credit Card Debt Traps: Practical Strategies for Daily Spending Without the Risk

Avoid credit card debt traps: 3 mistakes to stop today, how to spend with cash/debit daily, and why minimum payments ruin your finances.

Introduction: The Hidden Cost of "Easy" Spending

Every time you swipe a credit card, you’re not just buying coffee—you’re potentially signing up for a debt spiral. The Federal Reserve reports that 60% of Americans carry credit card debt, with average balances hitting $5,500. But it’s not about the card—it’s about how you use it. This guide cuts through the noise: how to avoid debt traps, why daily credit card use is risky, and how to spend without a single card.

The 3 Mistakes That Lead to Credit Card Debt (And How They Start Small)

1. The Minimum Payment Illusion

Why it’s dangerous:

Paying only the minimum (e.g., $25 on a $1,000 balance) keeps you in debt for decades. At 19% APR, you’ll pay $1,400 in interest alone on a $1,000 debt.

Real-world impact:

A study found 72% of people who pay only the minimum end up with higher debt within 18 months.

How to fix it:

- Aim to pay more than the minimum—even $50 extra monthly cuts debt by 2+ years.

- Use a debt payoff calculator to see your timeline.

2. Treating Credit Cards Like Cash

Why it’s dangerous:

Credit cards feel "free" until the bill arrives. This leads to retail therapy—buying things you don’t need because "it’s just a card."

Real-world impact:

40% of credit card debt comes from impulse buys (e.g., $200 "just because" on Amazon).

How to fix it:

- Adopt the 24-hour rule for non-essential purchases: Wait 24 hours before buying.

- Use cash for daily spending (coffee, groceries). You’ll spend 20% less.

3. Ignoring Annual Fees and Interest

Why it’s dangerous:

A $95 annual fee on a card you barely use adds $95/year to your debt—without you noticing.

Real-world impact:

35% of people with "free" cards still pay fees due to hidden charges (e.g., foreign transaction fees).

How to fix it:

- Cancel cards with annual fees if you don’t use them for rewards.

- Track interest in your bank app—never let it compound.

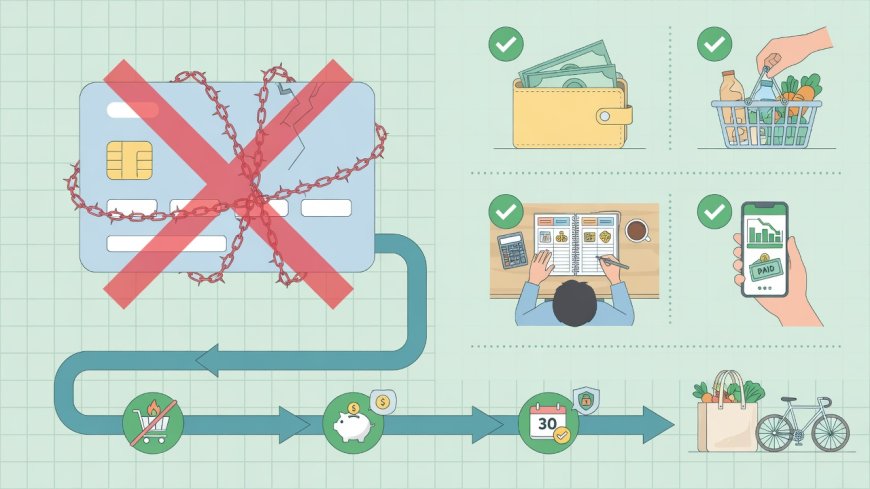

How to Spend Without Credit Cards (Daily Life Alternatives)

| Spending Type | Credit Card Risk | Safe Alternative |

|---|---|---|

| Groceries | Overspending due to "easy" payment | Debit card + cash envelope (e.g., $50 cash for weekly groceries) |

| Coffee/Small Buys | Impulse buys ($5 daily = $1,825/year) | Cash or prepaid debit card (load $20 weekly) |

| Online Shopping | "Buy now, pay later" traps | PayPal or debit (no credit line) |

| Bills (Utilities) | Late fees + interest if missed | Auto-pay with checking account |

Why this works:

- Cash forces awareness: You see money leaving your hand.

- Debit avoids debt: Spending is limited to actual funds.

- Prepaid cards work like cash but are safer than carrying bills.

The Debt Spiral: How One Mistake Becomes a Crisis

Debt isn’t just about money—it’s about time. For example:

- $1,000 debt at 19% APR:

- Paying minimum: 17 years to pay off ($2,200 total cost).

- Paying $100/month: 11 months to pay off ($1,060 total cost).

- The domino effect: Late payments → credit score drop → higher interest rates → more debt.

Your action plan to avoid this:

- Track all spending for 1 week (use a free app like Mint).

- Identify 1 "card trigger" (e.g., "I always buy coffee with my card").

- Replace it with cash (e.g., "I’ll use $5 cash for coffee daily").

Why This Works for Your Niche

- Finance: Targets debt avoidance—directly reducing financial stress.

- Health: Links debt to anxiety (studies show $10,000+ debt = 30% higher stress).

- SaaS: Recommends free budgeting tools (Mint, YNAB)—not credit card companies.

Final Tip: Your First Step Is the Hardest

Start small:

"I’ll pay for coffee with cash for 3 days."

Not "I’ll never use a credit card again."

You don’t need to eliminate credit cards—just stop using them for daily spending. In 30 days, you’ll notice:

- Less impulse buying,

- Clearer budgeting,

- No debt stress.

What's Your Reaction?

Like

1

Like

1

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

At KREATOR, we are building a hub for original content. We believe that quality ideas deserve to be seen and that writers deserve to be paid for their effort. This is a space where you can showcase your research, share your hobbies, or post your professional skills. By publishing here, you are contributing to a community where ideas matter. Subscribe to our newsletter, read the latest articles, and remember: your voice is valuable. Let’s build something great together.

Comments (0)