Decoding Health Insurance: What "In-Network" and "Out-of-Pocket" Really Mean

Decoding Health Insurance: What "In-Network" and "Out-of-Pocket" Really Mean

You've spent weeks researching, compared plans, and finally picked a health insurance option. Congrats! But now you're left staring at terms like "in-network," "deductible," and "out-of-pocket maximum." It feels like learning a new language, and frankly, it's stressful. Understanding these terms isn't just about paperwork; it's about knowing when you can get care without breaking the bank.

Let's break down two of the most crucial (and confusing) terms: In-Network and Out-of-Pocket.

What Does "In-Network" Really Mean for You?

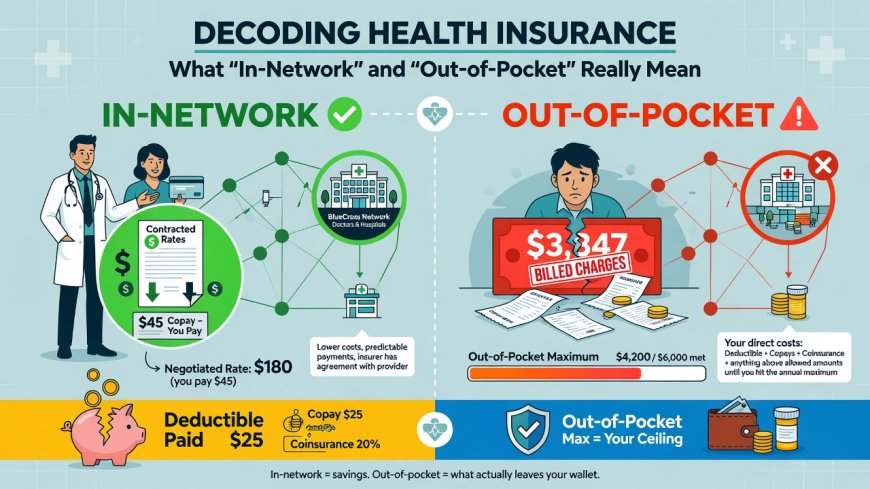

Think of "in-network" as your approved inner circle for healthcare providers – doctors, hospitals, specialists, labs, etc. They've signed a contract with your insurance company to provide care under agreed-upon prices.

- Why It Matters (The Benefit):

- Lower Costs: When you see an in-network doctor, your copay (the small fee per visit) or coinsurance (a percentage you pay after the deductible) is typically much lower than seeing an out-of-network provider.

- Predictable Spending: Your insurance will pay a larger share of the costs for in-network visits, making it easier to budget and understand your medical expenses.

- What Does It Mean (The Responsibility):

- Stick to Your List: Your insurance provides you with a list of in-network providers (or you can search). To maximize your benefits and minimize costs, try to choose doctors and hospitals from this list. Think of it like using your preferred grocery store brand – often cheaper and you know the price.

- Potential Limitations: Sometimes, you might genuinely need to see an out-of-network doctor (e.g., a specialist not contracted with your plan). Don't be afraid to ask about options first. But be aware that costs will likely be higher.

What Does "Out-of-Pocket" Actually Cost You?

This term refers to the money you personally spend on your healthcare after your insurance has started paying. It's the total you pay before your insurance's "out-of-pocket maximum" stops paying.

- Key Components (How You Pay):

- Deductible: The amount you pay for covered services before your insurance starts to pay. (E.g., You might pay 100% of costs until you meet your deductible.)

- Copay: A fixed amount you pay for a specific service (like a doctor's visit) when you see an in-network provider.

- Coinsurance: A percentage you pay for covered services after you've met your deductible (or sometimes instead of a copay).

- The Safety Net (Out-of-Pocket Maximum): This is your absolute maximum for covered services in a plan year. Once you hit this limit, your insurance pays 100% of eligible costs for the rest of the year. It's designed to protect you from catastrophic medical bills.

Putting It Together (A Simple Example)

Imagine you have a health insurance plan with a deductible of $1,000, a copay of $30 for in-network doctor visits, and 20% coinsurance after the deductible. You see an in-network doctor for a check-up.

- First Visit (Deductible): You pay the $30 copay. Your deductible is still $970 away from being met.

- Later, You Get Sick (Deductible Not Met): You see the same doctor for an illness. You pay the $30 copay. You might also pay the doctor's fee directly (beyond the copay/coinsurance). Your insurance pays 80% (because you haven't met your deductible yet). Your deductible gets closer.

- After Deductible is Met: You meet your $1,00'th deductible. Now, for covered services, you pay the 20% coinsurance. If you need more care, you pay your share (coinsurance) until you reach the out-of-pocket maximum.

The Takeaway: Know Your Terms, Know Your Costs

Understanding "in-network" and "out-of-pocket" isn't just about understanding policy documents; it's about navigating healthcare confidently. Knowing who is cheaper, how much you might need to pay for different scenarios, and what the ultimate safety net is, empowers you to make informed decisions about your health and your wallet. Don't be afraid to ask your insurance company to clarify terms – clarity is key to managing your healthcare effectively.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

At KREATOR, we are building a hub for original content. We believe that quality ideas deserve to be seen and that writers deserve to be paid for their effort. This is a space where you can showcase your research, share your hobbies, or post your professional skills. By publishing here, you are contributing to a community where ideas matter. Subscribe to our newsletter, read the latest articles, and remember: your voice is valuable. Let’s build something great together.

Comments (0)