Which Medicare Advantage Plan is Right for Your Budget and Health Needs?

HMO vs. PPO vs. EPO: Which Medicare Advantage Plan is Right for Your Budget? Meta Description: Still confused by insurance acronyms? We break down HMO, PPO, and EPO plans for Medicare. Learn which structure fits your budget and health needs best.

Let’s be real: Health insurance terminology can feel like learning a new language every time you read a brochure. But if you’ve ever stood in front of the Medicare Advantage selection screen, feeling like the options are endless and the terms are scary, you’re not alone.

You have Original Medicare, then you have the Medicare Advantage choices. And within those Advantage choices, you’ll see acronyms like HMO, PPO, and EPO.

They sound similar, but they work very differently. And the right choice depends less on what the acronym stands for and more on how you live your life.

Today, we are going to strip away the jargon and talk about your budget, your doctors, and your freedom.

The Three Main Players: What Do These Acronyms Mean?

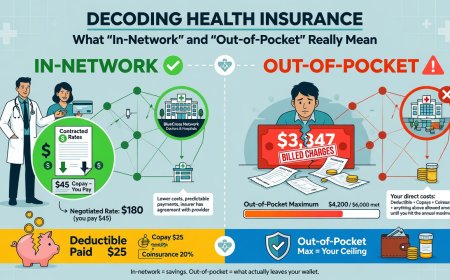

To pick the right one, you first need to know what they promise. Think of insurance networks like a club or a family reunion.

1. HMO (Health Maintenance Organization)

- The "Family Reunion" Rule: You usually must use doctors within the network.

- Referrals Required: If you want to see a specialist (like a cardiologist), your Primary Care Physician (PCP) usually has to say okay first.

- Costs: Often lower premiums and lower copays.

- Out-of-Network: Generally, you pay nothing, unless it’s a life-threatening emergency.

- Best For: People who see their PCP regularly, have a primary doctor, and want to save money on premiums.

2. PPO (Preferred Provider Organization)

- The "VIP Pass" Rule: You can see anyone you want.

- Referrals Not Needed: You can book an appointment with a specialist directly, even if you don't have a referral.

- Costs: Higher premiums. You might pay more in copays.

- Out-of-Network: You can go out of network, but you will pay more. You have to pay the difference between what the provider charges and what Medicare pays.

- Best For: People who see specialists often, travel frequently, or just want the freedom to change doctors easily.

3. EPO (Exclusive Provider Organization)

- The "Strict Guest List" Rule: You must use providers in-network, except for emergencies.

- Referrals: Usually not needed for specialists (like a PPO).

- Costs: Often sits between an HMO and a PPO in cost.

- Out-of-Network: Very strict. You generally won't be covered unless it’s an emergency.

- Best For: People who want the simplicity of a PPO (no referrals) but with the savings of an HMO (lower premiums), provided they don't travel often.

The Budget vs. Freedom Dilemma

This is where your "real world" life kicks in. Which one should you choose? Let's look at the trade-offs.

If You Choose HMO

The Trade-off: You get lower costs and simplicity, but you must stay in the network.

- Budget: Great for those who want predictable, low monthly bills.

- Health Needs: Ideal if you don't have a specific condition requiring outside specialists or if your doctor is already in-network.

- The Risk: If your favorite specialist retires, or you go to a hospital out of town, coverage might be tricky.

If You Choose PPO

The Trade-off: You get total freedom, but you pay a premium for it.

- Budget: The monthly plan cost might be higher. However, if you have a pre-existing condition that requires complex specialists, the flexibility might save you money later (by avoiding referral hassles or travel issues).

- Health Needs: Best if you have multiple specialists or travel for vacation/work.

- The Risk: If you don't use the network, costs spike.

If You Choose EPO

The Trade-off: No referrals, but no out-of-network access.

- Budget: A middle ground. Good for saving on the monthly premium without the hassle of referrals.

- Health Needs: Good if you want a direct path to specialists without the "approval" wait time of an HMO.

A Quick Decision Checklist

Before you enroll, run through this quick checklist to see which model fits your life.

| Question | HMO | PPO | EPO |

|---|---|---|---|

| Do I like my current Primary Care Doctor? | Yes (Must stay in network) | Yes/No (Network recommended) | Yes (Must stay in network) |

| Do I see specialists often? | No (Need referral) | Yes (No referral needed) | Yes (No referral needed) |

| Do I travel out of state? | No (Limited) | Yes (Partial coverage) | No (Limited) |

| Is my Budget Tight? | Good (Low premiums) | Maybe (Higher premiums) | Good (Low premiums) |

What About Emergencies?

A common fear is: "What if I break a leg on vacation?"

In all three plans (HMO, PPO, EPO), you are covered for emergencies, even out of network. However, there is a catch:

- PPOs often have a lower out-of-pocket cost for emergencies if you go out of network than HMOs/EPOs.

- HMOs & EPOs usually only pay for emergency services (like the ER), and then you might get a bill for non-emergency care if you don't return to your home network.

The Bottom Line

There is no "perfect" plan for everyone. There is only the plan that fits your doctor list and your wallet.

- If you are an HMO person: Stick with a PCP.

- If you are a PPO person: Value your independence.

- If you are an EPO person: Check the Network strictly.

Whichever you choose, read the Evidence of Coverage (EOC) document. It’s boring, but it will tell you exactly what happens if you choose the wrong doctor.

Disclaimer: Insurance plans and rules change annually. Always review your specific plan documents on Medicare.gov or with a licensed agent before making a final decision. This blog post is for educational purposes and not medical or financial advice.

Frequently Asked Questions

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

At KREATOR, we are building a hub for original content. We believe that quality ideas deserve to be seen and that writers deserve to be paid for their effort. This is a space where you can showcase your research, share your hobbies, or post your professional skills. By publishing here, you are contributing to a community where ideas matter. Subscribe to our newsletter, read the latest articles, and remember: your voice is valuable. Let’s build something great together.

Comments (0)