How to Choose Between Original Medicare and Medicare Advantage

Let's be honest: talking about health insurance can feel like walking through a maze with no map. Between the Part A and Part B terminology, the extra "Part D" for prescriptions, and the constant changes in coverage rules, it’s easy to feel like you’re drowning in paperwork.

But here is the good news: You don’t have to be an insurance expert to make the right choice.

If you are approaching the Annual Election Period (AEP)—or known as Open Enrollment—right now, you are standing at a crossroads. Do you stick with the safety net of Original Medicare, or do you bundle your benefits into a Medicare Advantage plan?

We’re here to help you navigate this. No jargon, no pressure, just clear answers to help you sleep better at night.

First, What Is the "Open Enrollment" Period?

Before we dive into the what and why, let's talk about the when. The Annual Election Period typically runs from October 15 to December 7. During this window, your coverage changes will take effect on January 1.

This is your time to pause, review, and potentially switch.

Quick Tip: There are specific enrollment windows, but if you are currently on Medicare, keep an eye on your local state-specific dates, as they might have a few extra nuances. However, for most seniors, Oct 15 – Dec 7 is the main event.

The Big Showdown: Original Medicare vs. Medicare Advantage

This is where most people get stuck. Both are government-approved ways to get your basic hospital and medical coverage. But the experience is vastly different. Let's break it down like we're chatting over coffee.

1. Original Medicare (Part A & Part B)

Think of this as the standard government-backed option. It's the "classic" way to do it.

- How it works: You pay your premium directly to Medicare (usually small, often $0 for Part A). You get Part A (Hospital) and Part B (Doctor/Outpatient). You can add a Part C (Medicare Advantage) or a Medigap (Supplement) plan for extra coverage.

- The Good:

- Flexibility: You can see any doctor or specialist in the country who accepts Medicare.

- Predictability: The costs are generally set by the government. What you pay for hospital stays is consistent.

- Travel: No "network" restrictions when you're on vacation.

- The "But":

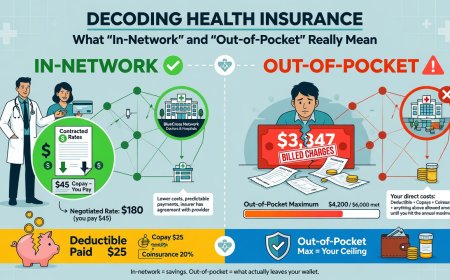

- Gaps: There are "coverage gaps." For example, Original Medicare doesn't cover hearing aids, dental, or vision. To cover those, you need to buy extra Medigap plans (which can be expensive).

- Out-of-Pocket: Without a Medigap, you could end up paying a lot if you have a major health event.

2. Medicare Advantage (Part C)

This is where private insurance companies step in to offer a "bundled" plan.

- How it works: Instead of getting coverage from Medicare directly, you get it through a private company that contracts with the government. It usually bundles Part A, Part B, and Part D (Prescriptions) into one plan.

- The Good:

- All-in-One: Often includes prescription drugs, dental, vision, and hearing coverage.

- Predictable Costs: These plans usually have an "out-of-pocket maximum." This means if you go to the doctor all year, you stop paying once you hit that limit.

- Perks: Many plans offer gym memberships, wellness programs, and over-the-counter drug allowances.

- The "But":

- Networks: You usually need to stick to a specific list of doctors and hospitals (like a standard HMO or PPO network). If you see an out-of-network doctor, you might pay more.

- Annual Changes: The plan's rules and costs can change every year. What was good for you last year might look different in January.

So, How Do I Choose? A Checklist for You

Choosing isn't about picking the "best" plan. It's about picking the plan that fits your life right now. Ask yourself these questions before clicking "Enroll."

The "Doctor Friendliness" Test

- Original: "I have a specialist I see every year. Can I see them?" -> Yes.

- Advantage: "Is that specialist in my network?" -> Check the plan's directory. If your specialist isn't there, that's a dealbreaker.

The "Prescription" Reality Check

- Original: You pay for drugs via Part D separately.

- Advantage: Usually includes Part D. However, check the formulary (drug list). Some Advantage plans don't cover the exact brand of medicine your doctor prescribes.

The "Traveler" Factor

- Do you take trips out of state? Original Medicare travels easier. Some Advantage plans only cover you in their service area.

The "Budget" Question

- Can you afford the extra cost of a Medigap plan to cover Original Medicare's gaps? If you want an all-in-one payment that includes dental/vision, Advantage might feel more secure.

The "Common Sense" Rules for Open Enrollment

As a senior, you are the expert on your life. But, as you navigate this, keep these common pitfalls in mind:

- Don't let the pressure rush you. Just because a salesman calls you doesn't mean you have to buy a plan right this second. It's okay to compare quotes.

- Watch out for "Gaps" in coverage. If you are on Advantage, make sure you know exactly what happens when you hit your deductible.

- Review the plan every year. Medicare Advantage plans can change their benefits annually. If your doctor leaves or a drug goes off the list, your plan might need to change.

A Note on the Future (And Your Peace of Mind)

We know it feels stressful. You are worried about your health, your finances, and your loved ones.

Remember: Medicare is there to support you, not to hold you hostage. You can change plans, and if you have questions, ask them. If you are unsure, talk to a licensed broker who isn't selling a specific product (unbiased advice is valuable).

By understanding the differences between Original and Advantage plans, you take back control of your health journey. Whether you choose the flexibility of Original Medicare or the bundled benefits of Advantage, the goal is the same: You want coverage that lets you focus on living, not filling out forms.

Happy Enrolling!

Disclaimer: This blog post is for informational purposes only and does not constitute financial or medical advice. Medicare rules can change, and individual health needs vary. Please consult with a licensed insurance professional or visit the official Medicare.gov website for the most current information.

Frequently Asked Questions

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

At KREATOR, we are building a hub for original content. We believe that quality ideas deserve to be seen and that writers deserve to be paid for their effort. This is a space where you can showcase your research, share your hobbies, or post your professional skills. By publishing here, you are contributing to a community where ideas matter. Subscribe to our newsletter, read the latest articles, and remember: your voice is valuable. Let’s build something great together.

Comments (0)