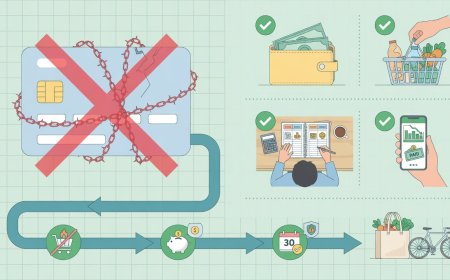

30‑Day Debt‑Free Challenge: Step‑by‑Step Plan

Want to start your financial journey today? Join the 30‑Day Debt‑Free Challenge. Includes specific steps, financial goals, and the best tools to conquer high‑interest debt fast.

Let’s be brutally honest for a second.

If you have a mortgage, a car loan, and student loans, paying off everything in 30 days isn't happening. That’s mathematically impossible without selling your home.

But here is the good news: You can clear high-interest revolving debt, stop the bleeding, and build serious momentum in just 30 days.

This isn't just about paying a bill; it's about changing your psychology. By the end of this month, you won't just be "less in debt." You will be in control. You will know exactly where every dollar is going. You will wake up knowing that one more hurdle is gone.

Welcome to the 30-Day Debt-Free Challenge. Here is how you execute it, the goals you need to hit, and the tools you'll need to succeed.

Why Do a 30-Day Challenge?

Most people wait for New Year's Resolutions to work on their finances. That's a mistake.

Debt snowballs don't wait. Interest doesn't sleep. Every day you delay payment on a high-interest credit card, you lose. This challenge forces you to pause, evaluate, and act.

- Day 1: Stop the bleeding.

- Day 10: Pay off your first "small" debt (the Snowball method).

- Day 30: Celebrate momentum and set the next phase.

Phase 1: The Audit (Days 1–5)

You can't fight a monster you can't see. Before you move money, you need to map the battlefield.

Step 1: List Every Single Debt

Stop using the "big picture" mental math. Open a spreadsheet and list:

- Creditor Name

- Total Balance

- Interest Rate (APR)

- Minimum Monthly Payment

- Statement Due Date

Goal: Have a complete, honest debt inventory within 48 hours. Tool: Google Sheets, Excel, or a Debt Snowball Calculator online.

Step 2: The "Pause and Pray" Strategy

Stop spending. Not even a dollar of non-essentials. No coffee, no dining out, no impulse buys. Redirect every single dollar that usually goes there directly to debt.

Goal: Eliminate all new discretionary spending. Tool: A tracking app like YNAB or a simple "Penny Jar" system.

Step 3: Choose Your Weapon

There are two main schools of thought:

- The Debt Avalanche: Pay highest interest rate first. Mathematically cheapest.

- The Debt Snowball: Pay smallest balance first. Psychological win (quickest win).

Goal: Choose one strategy and stick to it. Tool: A "Debt Priority List" where you circle the target debt daily.

Phase 2: The Attack (Days 6–20)

This is where the rubber meets the road. You are going to make aggressive payments.

Step 4: Slash the Expenses

Audit your last 3 months of bank statements.

- Is that subscription service still needed?

- Are you using a cheaper alternative for groceries?

- Can you negotiate your rates?

Goal: Free up at least 10–20% of your monthly budget for debt. Tool: Budgeting apps like Monarch Money or even a simple pen and paper log.

Step 5: The "Surplus" Payment

Take every cent of extra income (bonuses, tax refunds, or cash from selling old stuff) and throw it at your target debt.

Goal: Pay off one credit card balance entirely by Day 14. Tool: Cash or check for manual payments (sometimes feels more impactful than auto-pay).

Step 6: Debt Consolidation Check

If you have multiple cards with 20%+ APR, ask about a Balance Transfer or Consolidation Loan.

- Warning: Only do this if you won't be tempted to use the cards again.

- Goal: Reduce total APR of your target debt by at least 5%. Tool: Credit card balance transfer calculators.

Phase 3: The Lock-In (Days 21–30)

Now that you've paid something off, you have to make sure you don't go back.

Step 7: Build the Emergency Fund

If your emergency fund is zero, put a small amount (e.g., $1,000) there. Otherwise, the next shock will take you back to debt.

Goal: Save $1,000 "Starter Fund." Tool: High-Yield Savings Account (HYSA).

Step 8: Update Your Budget

Now that you have cash to pay off, you have more money left. Adjust your budget to reflect the new payment schedule.

Goal: Ensure the new budget covers debt + basic living. Tool: 50/30/20 Rule template.

Step 9: Plan for the Next Target

Look at your list again. What is the next small debt? Schedule it.

Goal: Have a payment schedule written out for the next 3 months. Tool: Digital calendar reminders for due dates.

Your 30-Day Checklist

Use this list to track your progress.

| Day | Task | Completed? |

|---|---|---|

| 1 | List all debts and APRs | ☐ |

| 3 | Cancel 1 unused subscription | ☐ |

| 7 | Stop spending non-essentials | ☐ |

| 14 | Make a large lump sum payment | ☐ |

| 15 | Choose first debt to attack | ☐ |

| 21 | Celebrate small win | ☐ |

| 30 | Review savings and debt balance | ☐ |

Debt is a numbers game, but it's also a game of will.

By Day 30, you aren't just looking at a smaller number on your statement. You are looking at a better version of yourself. You saved money. You proved you have self-control. You built a habit that will serve you for the rest of your life.

Start today. Pick one debt. Make a payment. The future version of you is waiting to thank you.

Disclaimer: The information provided in this article is for educational purposes only and is not financial advice. Always consult with a qualified financial professional before making significant changes to your financial plan or debt repayment strategy.

Frequently Asked Questions

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Wow

0

Wow

0

Sad

0

Sad

0

Angry

0

Angry

0

At KREATOR, we are building a hub for original content. We believe that quality ideas deserve to be seen and that writers deserve to be paid for their effort. This is a space where you can showcase your research, share your hobbies, or post your professional skills. By publishing here, you are contributing to a community where ideas matter. Subscribe to our newsletter, read the latest articles, and remember: your voice is valuable. Let’s build something great together.

Comments (0)